Critical minerals: the who, what and why for Australia and New Zealand

Critical minerals seem to be the latest talking point, making their way into so many headlines and political speeches of late. Thanks to Geoscience Australia, a quick definition is:

A critical mineral is a metallic or non-metallic element that has two characteristics:

- It is essential for the functioning of our modern technologies, economies or national security.

- There is a risk that its supply chains could be disrupted.

As global supply chains learn—again—the fragility of geopolitical dependencies, Australia and New Zealand find themselves in a position both familiar and newly strategic: distant, yet politically stable caretakers of the minerals that help power cities, industries, defence, critical infrastructure, and far more.

Australia’s critical minerals deal with the US represents a historic step-change for local industry, creating enormous opportunities for organisations that provide and depend on them. Just this week, Australian Prime Minister Anthony Albanese and Canadian counterpart Mark Carney pledged to act as partners rather than rivals in critical minerals.

New Zealand has an equally important yet strategically different role to play, as the nation ramps up mining investment and capacity to capitalise.

The Australasia region is now being asked to play a more complex role: not just extracting minerals, but helping to build reliable, scalable and resilient supply chains that support the industries of the future.

That shift matters. Minerals essential to defence systems, data centres, renewable energy and advanced manufacturing are increasingly viewed as strategic assets, and supply reliability is becoming as important as geological abundance.

Critical minerals as a risk and governance issue

The growing focus on critical minerals reflects more than demand for new commodities, it exposes a convergence of risks that now sit at the core of mining sector decision‑making. Projects are increasingly characterised by higher technical complexity, tighter development timelines, greater regulatory scrutiny and heightened investor expectations around resilience and reliability. In this environment, critical minerals developments are not simply judged on resource quality or strategic alignment, but on how effectively organisations anticipate disruption, manage execution risk and govern long‑term operational performance.

Australia: A super producer rethinks its role

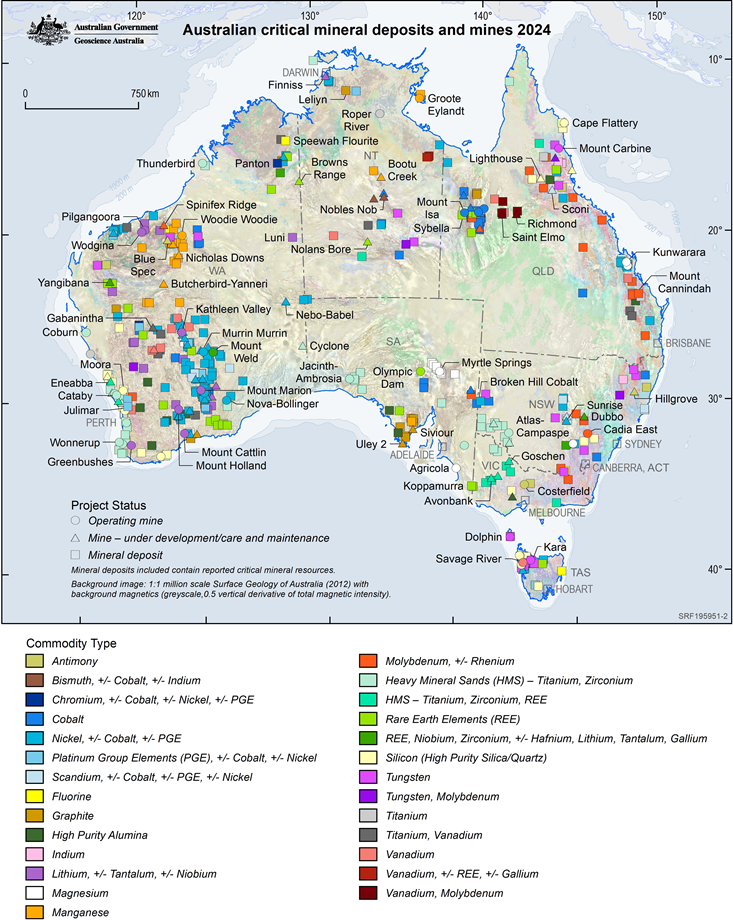

Australia is blessed with abundance. It’s a leading producer of lithium and cobalt and holds significant reserves of rare earths, gallium, antimony and other minerals essential to clean energy, defence, and high-technology manufacturing. Yet, for all its mineral wealth, Australia admits it doesn’t have a well-developed capability for processing or adding value to these raw materials.

Australia’s role has historically been weighted toward upstream extraction, with much of the downstream processing concentrated offshore. That equation is now changing. Policymakers are seeking to close processing gaps, reduce exposure to concentrated international bottlenecks, and position Australia as a trusted supplier within allied trade networks.

The federal government’s multiyear push has accelerated:

- The A$1.2bn Critical Minerals Strategic Reserve, announced in 2025 and planned for operation in late 2026, signals a pivot toward strategic stockpiling, price support mechanisms and sovereign capability, support mechanisms and sovereign capability.

- The updated Critical Minerals Strategy 2023–2030 and refreshed national list reinforce the priority placed on supply chain resilience and energy transition inputs, chain resilience and energy transition inputs.

These moves signal strongly that Australia aims to be investment-ready, processing-enabled, and geopolitically aligned. But that ambition brings new operational, technological, and resilience challenges as projects scale.

“As demand for critical minerals accelerates, geological opportunity alone will not determine success.”

New Zealand: A sector coming into focus

Across the Tasman, New Zealand’s critical minerals sector is smaller than Australia’s, but its strategic importance is growing quickly.

In early 2025, the government launched a national Minerals Strategy and a Critical Minerals List identifying 37 minerals essential to the economy, including newly elevated additions such as gold and metallurgical coal. It signals a clear shift toward expanding mining as an economic contributor, with an ambition to double mineral exports to NZ$3 billion by 2035.

Rather than competing on scale, New Zealand is positioning itself as a trusted, rules-based supplier of select minerals into global value chains. Minerals are typically designated as “critical when supply chains are exposed to disruption, particularly where processing and refining capacity is concentrated in a few locations. New Zealand’s emphasis on regulatory certainty and sustainability directly addresses this vulnerability.

What this means for leaders

For executives across mining, energy and infrastructure, the growing focus on critical minerals reflects more than demand for new commodities, it exposes a convergence of risks that now sit at the core of mining sector decision‑making. Projects are increasingly characterised by higher technical complexity, tighter development timelines, greater regulatory scrutiny and heightened investor expectations around resilience and reliability. In this environment, critical minerals developments are not simply judged on resource quality or strategic alignment, but on how effectively organisations anticipate disruption, manage execution risk and govern long‑term operational performance. That acceleration brings new risk considerations:

- Operational risk, from permitting delays to asset protection, grows if things like natural hazard exposure and political risk aren’t closely considered. hazard exposure and political risk

- Supply chain exposure increases as processing capacity expands and reliance on specialist equipment, reagents, and digital systems grows, as organisations make efforts to secure inputs that underpin multi-decade investments.

- Operational technology and cyber risk rise as AI-enabled equipment, automation and connected control systems are deployed during design and commissioning phases, creating a growing new attack surface (cyber-physical).

- Investor and sustainability scrutiny intensifies, with resilience, cyber preparedness and business continuity now seen as indicators of long-term project quality.

Resilience must be embedded from day one. Early industrial control system cyber assessments, integrated physical and digital risk reviews, and rigorous engineering-led loss prevention can materially reduce disruption risk as assets move from construction into operation.

FM’s experience supporting large-scale critical mineral processing and mining developments across the region repeatedly proves that projects that treat cyber, physical, and supply chain resilience as foundational design considerations are better positioned to secure capital, protect value and operate reliably over the long term.

As demand for critical minerals accelerates, geological opportunity alone will not determine success. Increasingly, outcomes and opportunities are shaped by how well organisations anticipate disruption, embed resilience into asset design and demonstrate credible oversight before issues arise. In Australia and New Zealand, the organisations that treat physical, digital and supply‑chain resilience as foundational will be better positioned to deliver reliable performance in an increasingly scrutinised operating environment.

GLOSSARY – The terms to know

Strategic minerals

Often used interchangeably with “critical minerals,” but usually implies national security importance (defence, geopolitics, alliances).

Criticality

A measure combining economic importance with vulnerability to supply disruption—often considering not just ore availability but processing bottlenecks, geopolitical concentration and specific industrial uses.

Critical Minerals Strategic Reserve (Australia)

A government backed reserve of key minerals, funded with A$1.2bn, designed to stabilise supply, intervene in markets when necessary and ensure domestic demand is met during disruptions. Operational from late 2026.

Value adding/processing

Downstream steps—refining, separation, chemical processing—that turn raw mineral concentrate into usable industrial inputs. Australia currently underperforms here but aims to grow this capability.

AUKUS

Security partnership (Australia–UK–US). Increasingly linked to critical minerals and defence supply chains.

Quad

Australia, US, Japan, India. Cooperation includes supply chain resilience, including minerals.

Critical Minerals List (NZ)

New Zealand’s formal list of 37 minerals considered essential to the nation’s economy, designed to guide investment, exploration and export strategy. Includes recent additions such as gold and metallurgical coal.

Minerals Strategy (NZ)

A long-term policy framework to 2040 focusing on productivity, value and resilience across land based, marine and recycling driven mineral production. Includes a goal to double exports to NZ$3bn by 2035.